A groundwater contamination plume is the body of polluted water that forms when contaminants reach the water table and move with the natural flow of groundwater. When a business owner or property owner receives a cleanup order referencing a plume, the scope of what regulators require, and what it will cost, is determined largely by the groundwater plume’s characteristics: how far it has traveled, how deep it has gone, what it contains, and how long it has been there.

This guide explains what a groundwater plume is, how it is found and characterized, how that information defines cleanup obligations, and what the plume itself can reveal about the financial resources that may be available to address it.

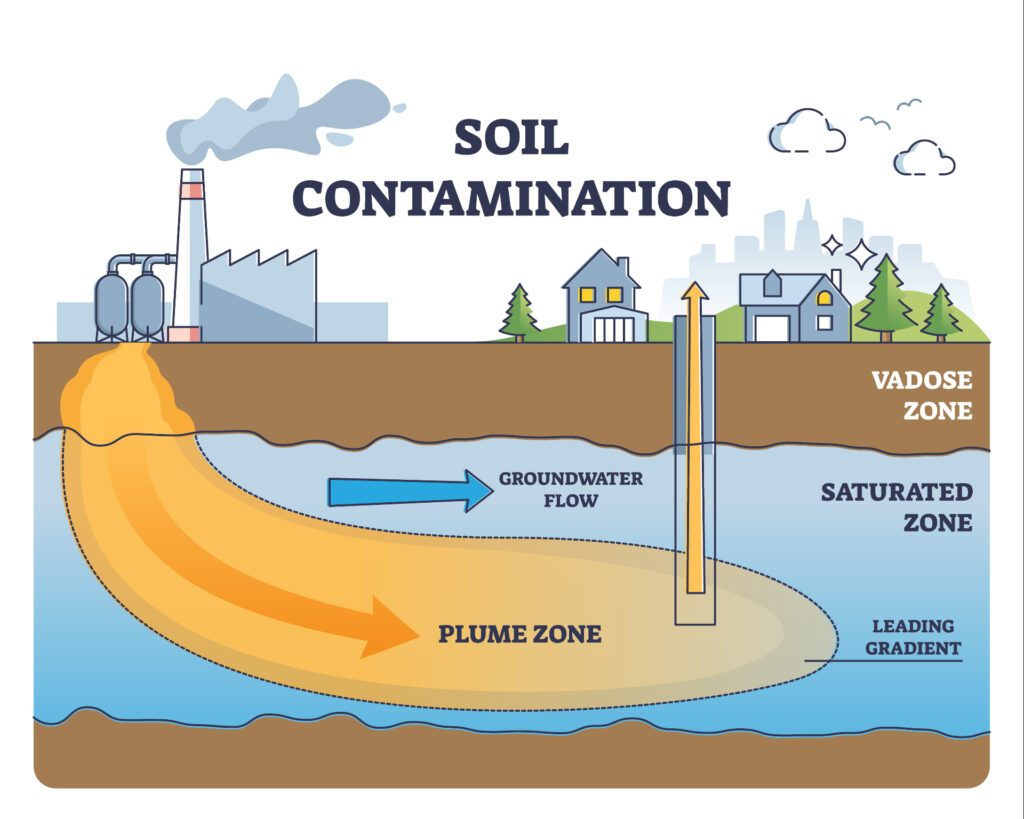

What Is a Groundwater Contamination Plume?

Think of groundwater as an underground river slowly seeping through a giant sponge. Rain and surface water filter down through soil and rock until they reach a saturated layer beneath the earth, known as the water table, where water fills every available space and moves gradually in the direction of the terrain’s natural slope.

When contaminants enter the ground, through a leaking storage tank, years of chemical disposal, industrial solvent use, or by some other means, they travel downward with that same water until they reach the saturated zone. Once there, they spread outward and continue moving with the flow of groundwater, forming what investigators call a plume: a traveling body of contaminated water migrating away from its source. Two components define it:

- The source zone is where the original release occurred. Residual contamination is often still present here, continuing to dissolve into groundwater long after the initial spill or leak.

- The dissolved plume is everything that has already traveled beyond the source, carried outward by groundwater flow. Think of it as dye dropped into a slow-moving stream: the point of entry is the source zone, and the spreading color moving downstream is the plume.

Because groundwater moves slowly and stays out of sight, contamination can travel for years or decades before anyone detects it. Discovery typically happens when something forces a closer look: a property sale, a redevelopment project, a regulatory inspection, or testing triggered by a neighboring site investigation.

How a Groundwater Plume Is Investigated and Characterized

Before a groundwater plume can become anyone’s legal or financial obligation, it has to be found and mapped. That process is called a site investigation, and it follows a defined sequence shaped by site-specific environmental factors, including soil composition, depth to groundwater, and the nature of the suspected contamination.

The typical entry point is a Phase II Environmental Site Assessment, which moves beyond the historical records review of a Phase I ESA to actual physical sampling of soil and groundwater. Investigators install monitoring wells at strategic locations to track the plume’s location, how far it has traveled, and how concentrated the contamination is at different points along its path. Techniques include soil borings, groundwater sampling, aquifer testing, and geophysical surveys. Multiple rounds of sampling are typically required before regulators have enough data to define the plume’s boundaries, identify its source, and establish how long it has been migrating, all of which feed directly into the cleanup obligation.

How a Groundwater Plume Defines the Scope of a Cleanup Order

The size and location of a groundwater plume determine what regulators will require. A plume contained within a single property is a different situation than one that has crossed a boundary into neighboring land or reached nearby water resources. The further the contamination travels, the broader and more expensive the cleanup obligation becomes.

When a plume migrates offsite, the stakes rise further. The responsible party can face liability for cleanup on land they don’t own and claims from affected neighbors. Under CERCLA, that liability can attach regardless of whether the current owner caused the contamination, meaning someone who purchased a property years after the original contamination release can still be held responsible for addressing it.

Once the plume’s extent is established, regulators require a soil and groundwater remediation plan. Some of the most widely used methods include pump-and-treat systems, which use extraction wells to capture and remove contaminated groundwater; in-situ chemical treatment, which breaks down contaminants underground without excavation; and monitored natural attenuation, where natural processes degrade contamination over time under regulatory oversight.

What the Characteristics of a Groundwater Plume Reveal About Your Situation

When an environmental investigation confirms a plume, the financial reality sets in quickly. Cleanup costs can reach into the millions, and the obligation often falls on whoever currently owns the property, regardless of who caused the problem.

What most property owners don’t realize is that the same plume data establishing their liability also contains information that may help address it. Its size, depth, behavior, contaminant type, and age each tell a distinct part of the story: where the contamination came from, why remediation costs what it does, who may ultimately be responsible, and what financial resources may exist to help pay for it.

Size

How far a groundwater plume has traveled and for how long reflects the scale of the cleanup obligation. That timeline matters beyond its implications for remediation scope. The longer a plume has been traveling, the more policy years may be available under historical insurance coverage to help fund the cleanup. A large plume isn’t only evidence of a serious problem. It may also be evidence of a larger pool of recoverable coverage.

Depth

How deep a plume has penetrated affects both the cost and the complexity of remediation. Shallow plumes in permeable soils are generally more accessible and less expensive to address. Plumes involving contaminants that are denser than water and sink well below the water table can require extensive extraction infrastructure and long-running treatment operations that drive costs into the millions.

Depth also provides a clue about what the contaminant is and how it has behaved over time, both of which help establish when contamination likely began and the coverage years that may apply.

Behavior

Different contaminants move through groundwater in distinct ways. Petroleum-based compounds tend to spread laterally near the top of the water table. Chlorinated solvents such as perchloroethylene (PCE) and trichloroethylene (TCE) are denser than water and sink through the saturated zone before spreading horizontally, often traveling further and persisting longer than petroleum-based plumes.

Understanding how a plume has behaved helps investigators estimate its age and trace it back to a source, both of which are critical inputs for building an insurance recovery argument. Where volatile compounds are present, vapors can also migrate upward into buildings above the plume, a phenomenon known as vapor intrusion that may require a separate response.

Type

Once behavior points toward a likely chemical class, the specific contaminant can often identify the source industry. For current property owners who did not cause the contamination, this is the first step toward establishing who did, which determines whose insurance history is relevant. Whether a dry cleaner operating in the 1970s, a gas station with a leaking underground storage tank, or a metal finishing operation, each leaves a chemical signature. Identifying that signature helps direct the search for historical coverage toward the right policyholder and the right policy years.

Age

The age of a groundwater plume is often the least understood characteristic and potentially the most financially significant. A plume that has been migrating for 25 years is not just evidence of a longstanding problem. It is a timeline that corresponds directly to the calendar years during which insurance policies were in force. Environmental investigation data that establishes when contamination likely began can identify which years are relevant.

For property owners who operated a business or held coverage during those years, that record of continuous contamination may be the key to unlocking insurance resources they didn’t know were still available to them.

How Historical Insurance Policies Can Fund Groundwater Cleanup

Commercial General Liability policies issued before the mid-1980s predate modern pollution exclusions, which means they may still respond to contamination claims today even when modern policies do not. Because these policies were occurrence-based, each year that a plume was actively migrating could represent a separate trigger with its own coverage limits. A plume with a 25-year migration history could correspond to 25 policy years, producing a cumulative pool of coverage that looks very different from what a single modern policy offers.

The challenge is that these policies are frequently lost or assumed to be gone entirely. Many can still be located with the help of insurance archaeologists who systematically search for and reconstruct historical coverage using carrier records, industry databases, and secondary evidence. The same investigation data that establishes when a plume began migrating becomes the foundation for that recovery argument. Coverage outcomes depend on the specific terms of each policy and the strength of available evidence, but determining whether historical coverage exists is a critical step before assuming cleanup costs must be paid entirely out of pocket.

Recover Cleanup Costs Through Restorical Research

Receiving a cleanup order tied to a groundwater plume is a serious financial event. Investigation costs, remediation expenses, and potential third-party liability can accumulate quickly, and the regulatory process moves on its own timeline regardless of whether funding is in place. What many property owners don’t realize is that the same plume data their environmental consultant is using to define the cleanup obligation may also be the foundation for an insurance recovery argument.

Restorical Research specializes in locating and reconstructing historical insurance policies for policyholders and property owners facing environmental cleanup obligations. Working exclusively on the policyholder side, Restorical analyzes coverage across policy years, identifies relevant carriers, and helps clients access funding that may have gone undiscovered for decades. Contact Restorical Research today for a free case review.